Risk is the likelihood of an undesirable event occurring with negative impact on your business and/ or family. It has the potential to harm both you and your business.

If you are a farmer, you are operating in a high-risk environment. Your crops are vulnerable to yield destruction due to drought, flood and storm. You face extreme market volatility driven by local and global supply-demand dynamics and trade policies.

Pests and diseases can wreak havoc, and they mutate into new forms that threaten your crops and livestock. Input costs for essentials like fertilis

er and fuel fluctuate widely due to exchange rates, trade agreements and subsidies.

Risk management

Risk management requires a structured approach, involving a cross-section of your staff with guidance from a professional in this field. Effective management involves identifying all the risks your business faces; estimating the probability of each occurrence; assessing the potential damage likely; and creating an action plan to mitigate its impact.

Risk registerThis involves listing the key risks facing your business, and ranking each based on the likelihood it will occur and the impact it could have.

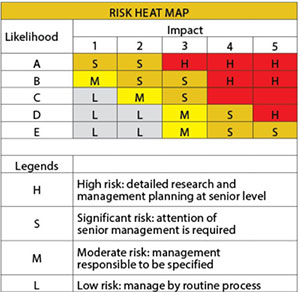

Risk heat map

From the risk register, the next step is to transcribe your findings into a ‘risk heat map’. This tool helps clarity priorities.

Red: high risk – requires immediate attention.

Orange: serious risk – needs attention but is less urgent.

Yellow: moderate risk – needs monitoring and management.

Grey: low impact – monitor, but

no special attention needed.

Final step: the action plan

There are only four options for dealing with risk. These are:

1. Avoid it by discontinuing the activity that causes it;

2. Reduce it by modifying operations;

3. Transfer it to someone else, such as an insurance company; or

4. Retain it, accept it, and prepare to manage the consequences.

Each option needs careful evaluation by someone capable of handling it. Your action plan will specify what needs to be done, who should do it, and by when it needs to be done.

Peter Hughes is a business and management consultant.