Platforms like Livestock Wealth are letting anyone from urban professionals to rural communities buy into cattle, blueberries, and macadamias, without owning a farm. The concept is compelling. But before you transfer funds, here is what you need to understand.

Imagine buying a pregnant cow. Not through a fund, not via a share certificate, but an actual animal, tagged and grazing on a commercial farm somewhere in South Africa. When she calves, the calf is grown out and sold. You receive a share of the proceeds. The cow herself may also be sold at maturity, generating a further return.

This is the premise of crowd-farming, and in South Africa, it is no longer a novelty. Platforms such as Johannesburg-based Livestock Wealth and Impact Farming from Fedgroup have drawn thousands of investors who are looking beyond the JSE for something they can understand, touch, and trace.

The appeal is real. So are the risks. And the regulatory picture, while clearer than it was two years ago, is still evolving. If you are considering putting money into cattle, trees, or farmland through one of these platforms, this is what you need to know.

Livestock Wealth was founded by Ntuthuko Shezi, who grew up in a community where cattle were not livestock but capital, a living store of value that could be leveraged for lobola, drawn on in tough times, and grown over generations.

“Where I grew up, cattle were never just animals. They were a measure of wealth, something on which you could rely. We wanted to create a way for anyone to participate in agriculture, even if they do not own land or have farming experience,” says Shezi.

How the model works

The digital platform translates that traditional model into a format accessible to anyone with a smartphone and a few thousand rands. Investors purchase a specific asset, a pregnant cow, a weaner calf, or a share in farmland, which is then managed by a vetted partner farmer for a defined production cycle.

Returns are not linked to interest rates or equity markets, but to biology: how the animal grows, how the calf performs, and at what price the asset is eventually sold. The platform manages onboarding, asset allocation, monitoring, and the final sale.

In practice, this places the platform in a hybrid role – part marketplace, part farm manager, part financial intermediary. But as the Financial Sector Conduct Authority (FSCA) has confirmed, the product is classified as an agricultural asset, not a financial instrument.

That distinction matters, and we will come back to it.

Beyond cattle: trees, blueberries, and macadamias

Livestock Wealth focuses primarily on cattle and citrus trees, but the crowd-farming model extends into perennial crops through players such as Fedgroup, whose Impact Farming platform allows investors to ‘own’ blueberry bushes, macadamia trees, or citrus trees on commercial farms.

These investments operate on longer time frames. A macadamia tree may take several years to reach peak production, but once established, they can offer more consistent annual yields than a single livestock cycle.

The trade-off is patience: capital is committed for longer, and exposure to input cost inflation, export market dynamics, and climate variability is ongoing rather than transactional.

For South African farmers, the relevance of these platforms is twofold. First, they represent an alternative funding channel, a way to bring in investor capital without taking on traditional debt. Second, for farmers with underutilised land or management capacity, becoming a platform partner can generate additional revenue.

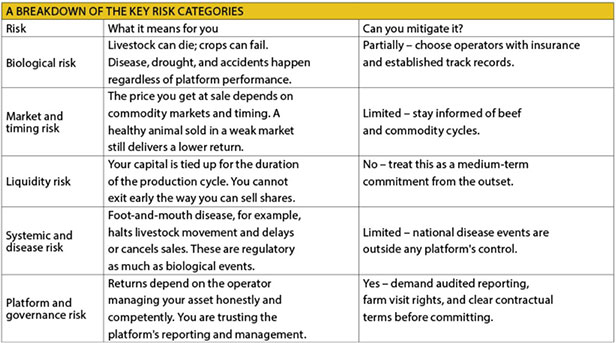

The risks every investor must understand

Crowd-farming platforms are effective at communicating upside. The language of ‘walking capital’, tangible assets, and agricultural heritage is compelling. But it can obscure the very real ways in which these investments can and do perform.

The biological risks deserve emphasis. Unlike a bond or a unit trust, an investment in a cow is an investment in a living system. Mortality, disease, failed pregnancies, drought stress, and poor veld conditions are not edge cases; they are the normal operating environment of South African commercial farming.

Shezi is direct about this: “You are working with nature. Unlike financial markets, you cannot fully control the outcome.”

Such honesty is admirable. Investors need to internalise it before committing capital.

The FSCA investigation: what happened and why it matters

In January 2024, the FSCA issued a public warning against Livestock Wealth, raising concerns that the platform may have been offering financial products without the appropriate licence under the Financial Advisory and Intermediary Services Act (FAISA) . The warning caused immediate investor anxiety and drew media attention.

After a full investigation, the FSCA found no fraud, no misappropriation of investor funds, and no evidence of a Ponzi scheme. Critically, it confirmed that the assets being offered, cattle and farmland, are agricultural assets, not financial products.

Because FAISA licensing requirements apply specifically to financial products and services, Livestock Wealth was found to be operating outside the scope of the Act and therefore did not require a financial services provider licence for this model.

“The investigation confirmed what we always said: we are providing access to real assets, not financial instruments. But hugging a cow is much more fun than holding a share certificate in your hands,” says Shezi.

The outcome was a significant regulatory vindication. But it also revealed something important about the landscape in which these platforms operate.

The regulatory gap and what may change

The FSCA investigation highlighted a structural issue that is not unique to Livestock Wealth: products that behave economically like investments are not always regulated as investments.

Because crowd-farming platforms deal in tangible assets rather than financial instruments, they fall outside the investor protection that FAISA provides, including requirements for disclosure, fit-and-proper conduct standards, and formal recourse mechanisms.

This is not necessarily a flaw in the platforms themselves. But it does mean that investors have fewer formal protection measures than they might expect, and that disclosure standards are voluntary rather than mandated.

The Conduct of Financial Institutions Bill (COFIB), expected to take effect later this year, may shift this. It proposes to regulate activities rather than products, meaning that platforms engaging in investment-like behaviour could become subject to oversight regardless of whether they deal in financial instruments or agricultural assets.

If enacted as drafted, this could standardise disclosure requirements, introduce conduct standards for platforms, and improve investor recourse.

Shezi acknowledges the direction things are going: “‘Regulation is catching up with innovation. We welcome clarity, as it will help build trust in the model.”

What to ask before you commit capital

If you are evaluating a crowd-farming platform, whether for cattle, trees, or farmland, these are the questions that matter:

- Who manages the farm and what is their history? Request verified production data, not just marketing material.

- Is the asset insured? What happens if the animal dies or the crop fails? Understand the loss scenario explicitly.

- What are the total fees? Understand the platform fee, the farmer’s share, and any ancillary costs before calculating your net return.

- What is the realistic return range, not the best case? Ask for historical performance data across multiple production cycles, not a single example.

- How long is my capital committed? Understand the production cycle length and what happens if the platform ceases to operate.

- Can I visit the farm? The ability to physically inspect your asset is one of the important distinctions between crowd-farming and conventional investing.

The bottom line

Crowd-farming platforms represent a genuine innovation in South African agricultural finance. They open farming to people who have never owned land, bring new capital into the sector, and reconnect urban investors with the biological realities of food production.

For farmers willing to take on management partnerships, these platforms can offer a supplementary funding stream with limited administrative burden.

But these are not passive investments. A cow is not a unit trust. A blueberry bush is not a bond. The assets live, grow, get sick, and respond to rainfall. Returns are variable by definition and depend heavily on the competence of the farmer managing your asset, someone you may never have met.

The FSCA’s clearance of Livestock Wealth confirmed the legitimacy of the model, but it did not make the underlying investment risk-free. As COFIB moves toward implementation, the regulatory environment for these platforms will tighten, bringing clearer disclosures and stronger protections, but potentially also higher compliance costs that could affect platform economics.

For now, the rule is simple: if you can afford to risk your capital, understand what you are buying, and are prepared to be patient, crowd-farming can be a meaningful addition to a diversified portfolio.

If you are counting on the return, treat it like what it is – an investment in something real, and reality is rarely predictable.

Farmer’s Weekly does not endorse any specific investment platform. This article is for information purposes only and does not constitute financial advice. Consult a registered financial adviser before making any investment decision.